How to Pick Travel Insurance for Railay or Tonsai Without Paying for the Wrong Plan

Match your Railay or Tonsai insurance to how long you are staying, how you move around, and whether you only need emergency protection or broader clinic access.

How to Pick Travel Insurance for Railay or Tonsai Without Paying for the Wrong Plan

Railay and Tonsai feel laid-back until something goes wrong and you have to leave the peninsula for treatment, pay a hospital deposit, or discover your policy did not cover the exact activity you assumed was normal. Insurance matters here because transport and treatment costs stack up fast once a simple accident stops being simple.

The biggest mistake is buying one cheap plan and assuming it covers every boat transfer, scooter ride, and clinic visit. A smarter approach is to check trip length first, then read the exclusions that matter most in southern Thailand, especially emergency-vs-routine coverage and motorbike engine-size limits.

Top 3 Travel Insurance Plans for Your Vietnam & Thailand Journey!

In this video, we dive into the top threetravel insuranceplans tailored for your adventures in Vietnam and Thailand. Whether ...

- Channel: The Adjutant 🇺🇸

Found a helpful clip from The Adjutant 🇺🇸 if you want to watch it on YouTube.

How to Pick Travel Insurance for Railay or Tonsai Without Paying for the Wrong Plan

Start with your trip length and real activity plan

A one-week beach stay does not need the same policy as a months-long Thailand base. Railay and Tonsai travelers often blur that line because a short trip can still include climbing, boat hops, kayaking, or scooter use on the mainland.

Write down what you are actually likely to do before comparing plans. Insurance only feels interchangeable when you stay vague about the trip.

- Count the real trip length, not just the peninsula nights.

- Note whether you expect climbing days, island hops, scooter rentals, or extended mainland time.

- Check whether your visa or long-stay plan changes the type of coverage you need.

Know the difference between emergency travel insurance and full health coverage

Travel insurance is usually there for emergencies: a crash, a serious illness, an evacuation, or a hospital event that would wreck the trip budget. It is not the same as broader health insurance that covers ordinary clinic use, follow-up visits, or ongoing care during a longer stay.

distinction matters if Railay or Tonsai is only one piece of a larger Thailand stay. The longer you remain in-country, the less useful an emergency-only mindset becomes.

- Use travel insurance for shorter stays built around emergency protection.

- Look at fuller health coverage when you expect regular care, prescriptions, or a long stay.

- Do not assume a policy that sounds global will handle routine clinic visits.

How to Pick Travel Insurance for Railay or Tonsai Without Paying for the Wrong Plan

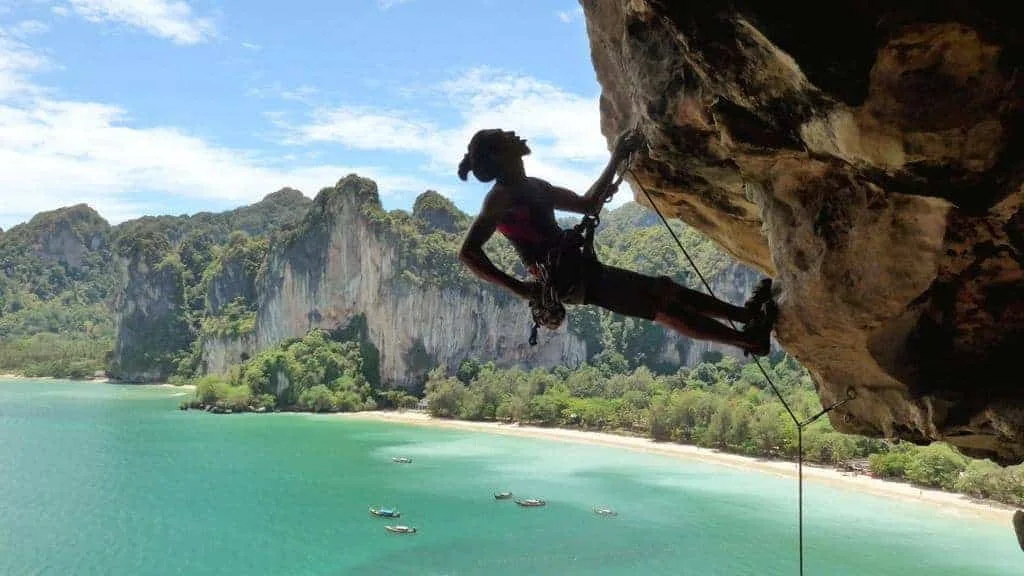

Read motorbike and activity exclusions before you trust the policy

This is the part travelers skip and regret later. Southern Thailand plans often look fine until you notice engine-size limits, licensing requirements, or activity exclusions that quietly remove the most common tourist accident scenarios.

Even if you plan to stay mostly on foot in Railay or Tonsai, many trips still involve scooter decisions before or after the peninsula segment. The policy needs to match that reality, not the ideal version of the trip.

- Check engine-size limits on motorbike coverage.

- Confirm whether climbing or guided activities need special wording.

- Make sure you understand the license and helmet requirements that affect claims.

Plan around hospital deposits and transfer logistics

A policy is only useful if it helps when a private hospital wants money up front or when you need treatment after leaving the peninsula. That is why emergency contact speed, reimbursement rules, and direct-billing expectations matter as much as the premium itself.

Railay and Tonsai are beautiful but not frictionless. If treatment starts with a boat ride and a mainland hospital desk, you want fewer surprises, not more paperwork confusion.

- Check whether the insurer offers direct billing or mainly reimbursement.

- Save the emergency number offline before the trip.

- Keep enough backup funds for deposits or transport while the claim process catches up.